Q1FY25 core operating profit of `9,637 crores up 16% YOY, NIM at 4.05%, cost growth moderating, aided by steady growth in average deposits and advances

Citi integration completed successfully in July 2024

*Bank’s focus segments include Small Business Banking (SBB), Small & Medium Enterprises, (SME), Mid Corporate, Rural, Personal Loans (PL) and Credit Card Advances

QAB: Quarterly Average Balance; MEB: Month End Balance; MAU: Monthly Active Users engaging in financial & non-financial transactions;

1 SBB : Small Business Banking;

2 Based on RBI data as of May’24;

3 Coverage Ratio = Aggregate provisions (specific + standard + additional + Covid) / IRAC GNPA;

^ Net accretion = capital accreted – capital consumed during the quarter

Snapshot (As on June 30th, 2024) (in ` Crores)

| Profit & Loss | Absolute (in ` Crores) | YOY Growth | QOQ | ||

|---|---|---|---|---|---|

| Q1FY25 | Q1FY24 | Q4FY24 | |||

| Net Interest Income | 13,448 | 11,959 | 13,089 | 12% | 3% |

| Fee Income | 5,204 | 4,488 | 5,637 | 16% | (8%) |

| Operating Expenses | 9,125 | 8,232 | 9,319 | 11% | (2%) |

| Operating Profit | 10,106 | 8,814 | 10,536 | 15% | (4%) |

| Core Operating Profit | 9,637 | 8,295 | 9,515 | 16% | 1% |

| Profit after Tax | 6,035 | 5,797 | 7,130 | 4% | (15%) |

| Balance Sheet | Absolute (in ` Crores) | YOY Growth |

|---|---|---|

| Q1FY25 | ||

| Total Assets | 14,68,163 | 13% |

| Net Advances | 9,80,092 | 14% |

| Total Deposits | 10,62,484 | 13% |

| Shareholders' Funds | 1,57,766 | 20% |

| Key Ratios | Absolute (in ` Crores) | |

|---|---|---|

| Q1FY25 | Q1FY24 | |

| Diluted EPS (Annualised in `) | 77.79 | 75.40 |

| Book Value per share (in `) | 511 | 425 |

| Standalone ROA (Annualised) | 1.65% | 1.80% |

| Standalone ROE (Annualised) | 16.26% | 19.17% |

| Cons ROA (Annualised) | 1.70% | 1.83% |

| Cons ROE (Annualised) | 16.68% | 19.44% |

| Gross NPA Ratio | 1.54% | 1.96% |

| Net NPA Ratio | 0.34% | 0.41% |

| Basel III Tier I CAR^ | 14.52% | 14.90% |

| Basel III Total CAR^ | 16.65% | 17.74% |

^ including profit after tax for Q1

13% YOY (a) 14% YOY (b)

13% YOY (a) 14% YOY (b)

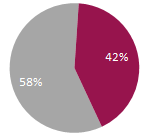

CASA

CASA

4% YOY (a) | 4% YOY (b)

(a) Month end balances (b) Quarterly average balance

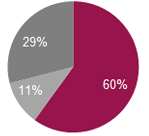

14% YOY (c) 15% YOY (d) Retail

Retail

SME

SME

Corporate

Corporate

18% YOY | 20% YOY | 6% YOY (c) 10% YOY (d)

(c) Overall (d) Overall (gross of IBPC sold)

16% YOY 4% YOY

Steady core operating performance

Loan growth delivered across focus business segment

MEB1 deposits grew 13% YOY; CASA ratio at 42%, which is amongst the best for peer private banks

Well capitalized with self-sustaining capital structure; adequate liquidity buffers

Continue to maintain strong position in Payments and Digital Banking

Asset quality stable, credit cost higher due to seasonality and lower recoveries and upgrades, not indicative of full year credit costs

Key domestic subsidiaries7 continue to deliver steady performance

1 MEB – Month End Balance,

2 Liquidity Coverage Ratio

3 with 2.7 mn+ reviews

4 Monthly active users, engaging in financial and non-financial transactions,

5 (specific+ standard+ additional + COVID)

6 Annualized

7 Figures of subsidiaries are as per Indian GAAP, as used for consolidated financial statements of the Group