IBPC: Inter Bank Participation Certificates

QAB: Quarterly Average Balance

MAU: Monthly Active Users engaging in financial and non-financial transactions

1 SBB : Small Business Banking

2 Based on RBI data as of Mar'24;

3 across 64 global banks, 82 fintechs and 9 neo banks with 2.6 mn+ reviews

4 Coverage Ratio = Aggregate provisions (specific + standard + additional + Covid) / IRAC GNPA

* Net organic accretion = capital accreted – capital consumed (excluding consumption for regulatory changes in risk weights)

Snapshot (As on March 31st, 2024) (in ` Crores)

| Profit & Loss | Absolute (in ` Crores) | QOQ | YOY Growth | |||

|---|---|---|---|---|---|---|

| Q4FY24 | Q3FY24 | FY24 | Q4FY24 | Q4FY24 | FY24 | |

| Net Interest Income | 13,089 | 12,532 | 49,894 | 4% | 11% | 16% |

| Fee Income | 5,637 | 5,169 | 20,257 | 9% | 23% | 28% |

| Operating Expenses | 9,319 | 8,946 | 35,213 | 4% | 27% | 30% |

| Operating Profit | 10,536 | 9,141 | 37,123 | 15% | 15% | 16% |

| Core Operating Profit | 9,515 | 8,850 | 35,393 | 8% | 5% | 10% |

| Profit after Tax | 7,130 | 6,071 | 24,861 | 17% | - | 160% |

| Balance Sheet | Absolute (in ` Crores) | YOY Growth |

|---|---|---|

| Q4FY24 | ||

| Total Assets | 14,77,209 | 12% |

| Net Advances | 9,65,068 | 14% |

| Total Deposits | 10,68,641 | 13% |

| Shareholders' Funds | 1,50,235 | 20% |

| Key Ratios | Absolute (in ` Crores) | |

|---|---|---|

| Q4FY24 / FY24 | Q4FY23 / FY23 (e) | |

| Diluted EPS (Annualised in `) | 92.34 / 80.10 | (75.53) / 31.02 |

| Book Value per share (in `) | 487 | 406 |

| Standalone ROA (Annualised) | 2.00% / 1.83% | (1.83%) / 0.80% |

| Standalone ROE (Annualised) | 20.35% / 18.86% | (19.20%) / 8.47% |

| Cons ROA (Annualised) | 2.07% / 1.84% | (1.68%) / 0.85% |

| Cons ROE (Annualised) | 20.87% / 19.29% | (17.37%) / 9.26% |

| Gross NPA Ratio | 1.43% | 2.02% |

| Net NPA Ratio | 0.31% | 0.39% |

| Basel III Tier I CAR | 14.20% | 14.57% |

| Basel III Total CAR | 16.63% | 17.64% |

(e) including exceptional Items on account of acquisition of Citibank India Consumer Business ('CICB')

13% YOY (a) 16% YOY (b)

13% YOY (a) 16% YOY (b)

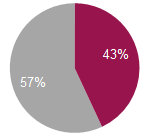

CASA

CASA

3% YOY (a) | 8% YOY (b)

(a) Month end balances (b) Quarterly average balance

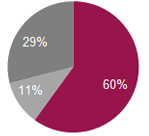

14% YOY (c) 15% YOY (d) Retail

Retail

SME

SME

Corporate

Corporate

20% YOY | 17% YOY | 3% YOY (c) 7% YOY (d)

(c) Overall (d) Overall (gross of IBPC sold)

16% YOY 160% YOY(e) including exceptional Items on account of acquisition of Citibank India Consumer Business ('CICB')

Strong operating performance

Healthy loan growth delivered across all business segments

Retail term deposits gaining traction, CASA ratio among the best in the industry

Well capitalized with self-sustaining capital structure; adequate liquidity buffers

Continue to maintain strong position in Payments and Digital Banking

Declining slippages, gross NPA and credit cost

Key domestic subsidiaries7 continue to deliver steady performance

1 QAB – Quarterly Average Balance,

2 Liquidity Coverage Ratio,

3 across 64 global banks, 82 fintechs and 9 neo banks with 2.6 mn+ reviews

4 Monthly active users, engaging in financial and non-financial transactions,

5 (specific+ standard+ additional + COVID)

6 Annualized

7 Figures of subsidiaries are as per Indian GAAP, as used for consolidated financial statements of the Group